Digital Health Market Outlook

Market Outlook

- After a strong performing Q1’25, global equity funding declined in Q2’25, with funding totaling $4.4B — a 21.4% decrease quarter-over-quarter.

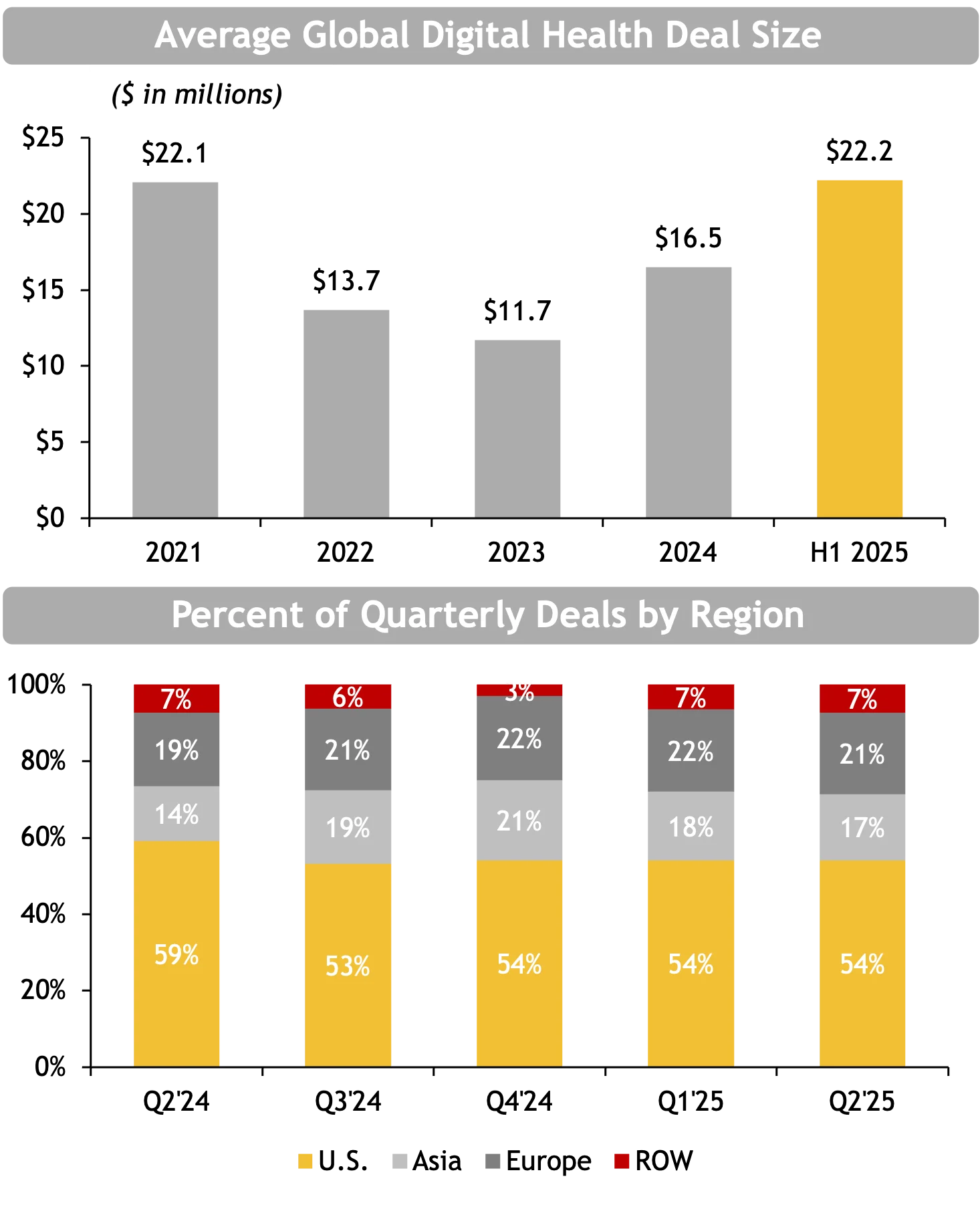

- Despite this decrease in funding, the average global deal size has increased from $15.5M in 2024 to $22.2M through H1’25, ultimately spurred by larger investments in later stage rounds as well as the bolstering impact of AI.

- Following a H1’25 that was driven by significant AI funding, increased provider tool adoption, and successful IPOs, investor sentiment remains positive for H2’25, with confidence in the sector’s continued growth and market maturity.

- The U.S. market share of funding remained the same in Q2’25 as it was in Q1’25, at 54%, reflecting a consistent level of investor interest. This stability may be attributed to ongoing optimism in the sector, bolstered by significant AI-driven investments and growing confidence in digital health’s long-term potential, despite broader economic and policy uncertainties.

- Among the quarter’s top fundraising deals were Neuralink’s $650M Series E round, led by G42 and Valor Equity Partners, and Pathos’s $300M Series D round led by undisclosed investors.

- Digital health M&A activity saw a slight decline from Q1’25 to Q2’25, as the number of M&A exits decreased from 50 to 43, respectively. The largest M&A deal of Q2’25 was Roper Technologies’ $1.85B acquisition of CentralReach, a provider of EHR, practice management, and clinical software focused on behavioral health practices.

Industry Snapshot

$4.4B

Global equity funding in Q2 2025

$22.2M

Average global deal size in H1 2025

54%

U.S. share of global digital health funding in 2025

43 M&A Exits

Down from 50 in Q1 2025, reflecting a slight dip in transaction activity

30%

Healthcare providers with full EHR interoperability achieved by 2025

80% faster

EHRs reduce the time required to access patient information